Exnet is a decision system.

- Dashboards

- Alerts

- Reporting layers

- Processes signals

- Produces decisions

- Routes actions

An intelligence layer for financial decisions.

Exnet transforms market, portfolio, client, and macro data into structured, execution-ready decisions — continuously, in real time.

Built by a team of data scientists, quant engineers, and finance professionals with experience across systematic investing, portfolio construction, and institutional workflows.

Our models are not theoretical. They are designed, tested, and deployed in the context of real financial decision-making.

This is not research. It is decision infrastructure.

Financial systems display data. They do not execute decisions.

- Display data

- Generate alerts

- Produce reports

- Manual, periodic, fragmented

- Markets move continuously

- Reviews happen periodically

- The gap widens between them

- Each delay compounds the next

- Large portfolios: systematic, continuous, quant-led

- Smaller portfolios: periodic, reactive, manual

- Same markets. Different infrastructure.

- Signals are modelled

- Risk is scored

- Decisions are systematic

- Capability existed. It wasn't accessible.

Exnet closes the gap between signal and action.

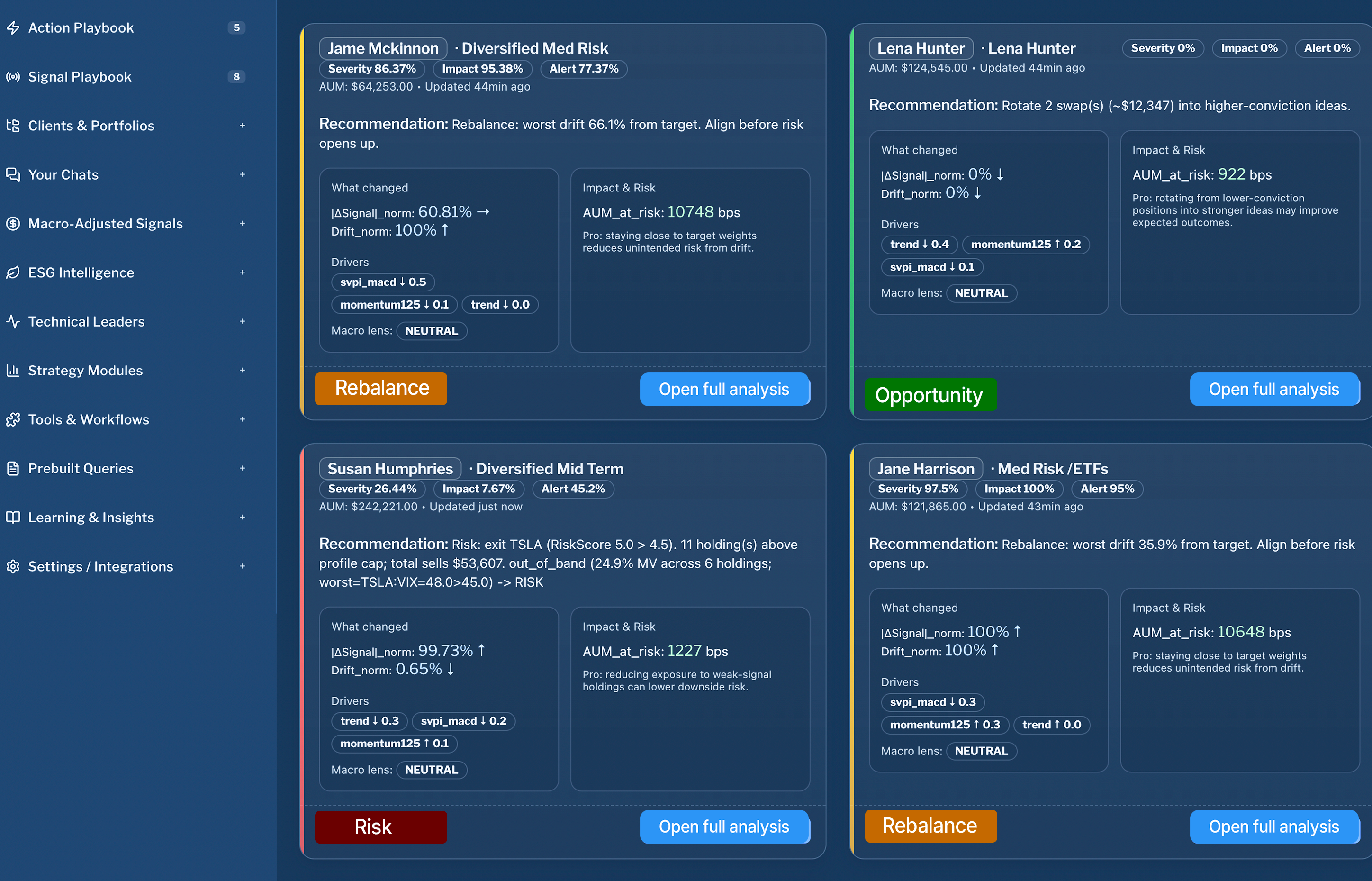

How the system operates.

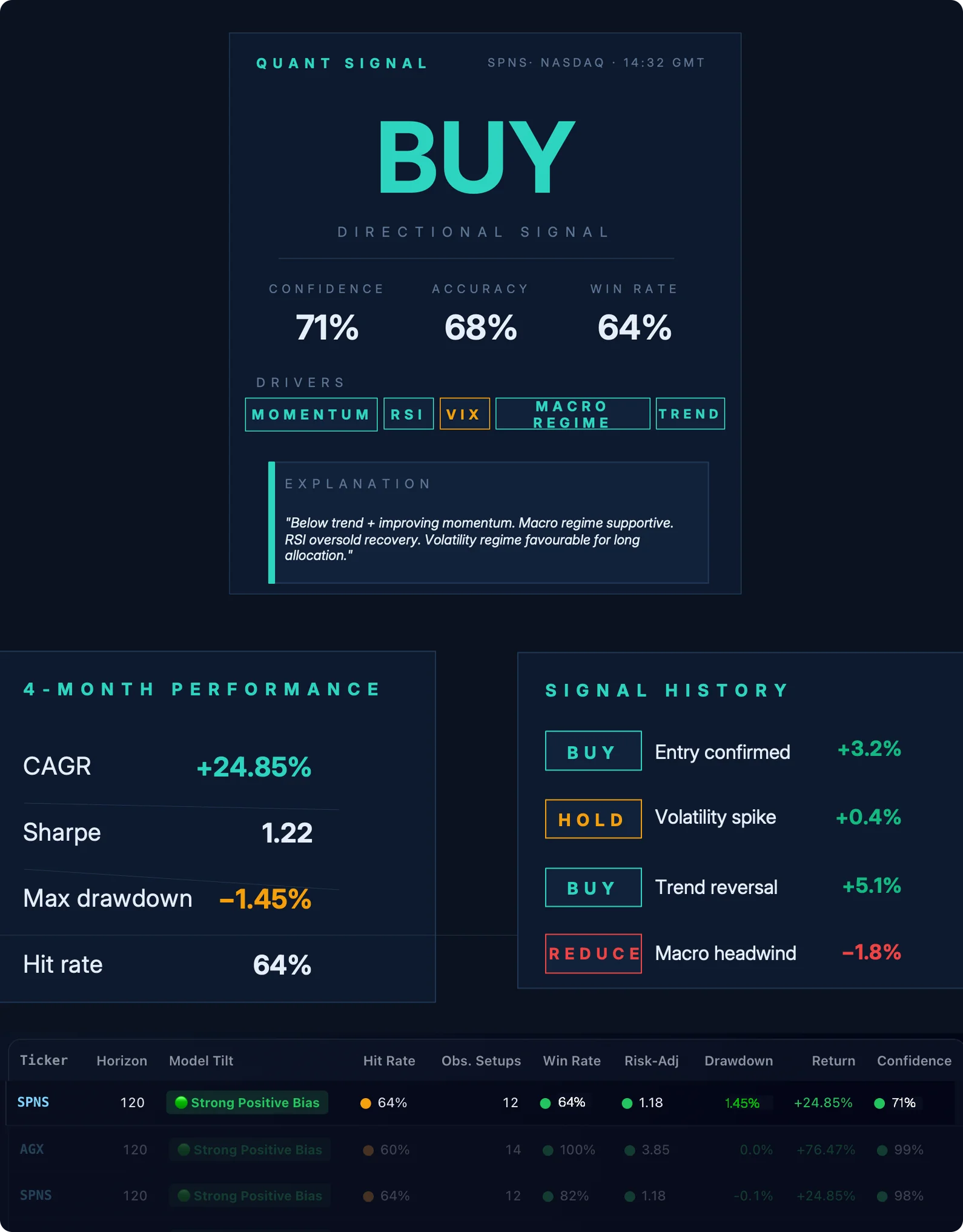

Detects signals

Market data, portfolio drift, regulatory triggers, ESG constraints, client events — ingested continuously.

Scores impact

Probability, urgency, confidence — each signal quantified, not described.

Prioritises decisions

Ranked by client exposure, not by alert frequency.

Routes actions

Advisor queue, automated transfer, compliance hold — execution-ready, not informational.

Models are validated. Not assumed.

Every scoring model is tested on historical data before deployment. Performance is measured on out-of-sample data across multiple horizons and regimes.

- rolling time splits

- no lookahead bias

- multi-horizon testing

- per-signal evaluation